Market Context: A Utility Turning Into a Capital Markets Play

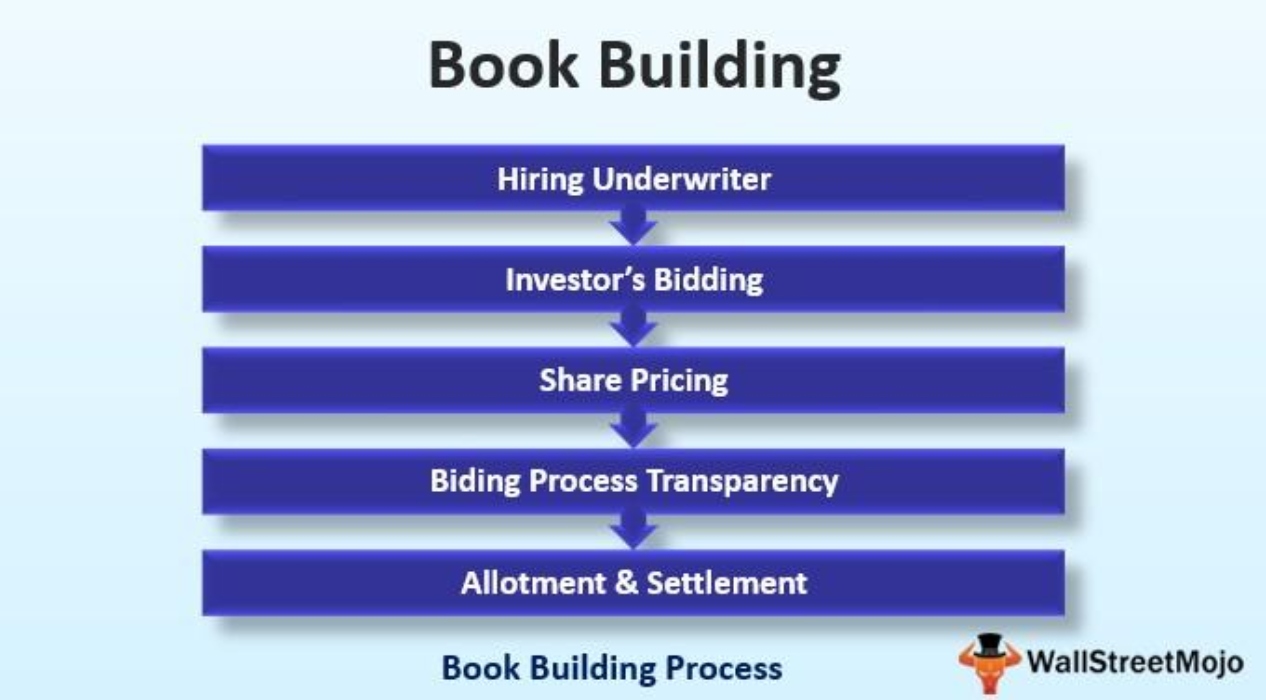

ADMIE (Independent Power Transmission Operator) is entering a decisive capital markets phase, with management intensifying investor outreach across Europe and North America ahead of a planned book-building process in London.

During recent roadshows, the dominant feedback from international asset managers and analysts was strikingly uniform: “Why are you not offering more equity?” — a signal interpreted by market participants as evidence of strong institutional appetite for regulated infrastructure exposure in Southern Europe.

The engagement included discussions with major global funds such as BlackRock, Lazard, and Fidelity, alongside a broader set of approximately 15 North American institutional investors.

The Investment Narrative: Regulated Cash Flow Meets Energy Transition

ADMIE’s pitch to investors is increasingly framed around three structural pillars:

- Long-duration regulated revenues supported by stable transmission tariffs through 2030

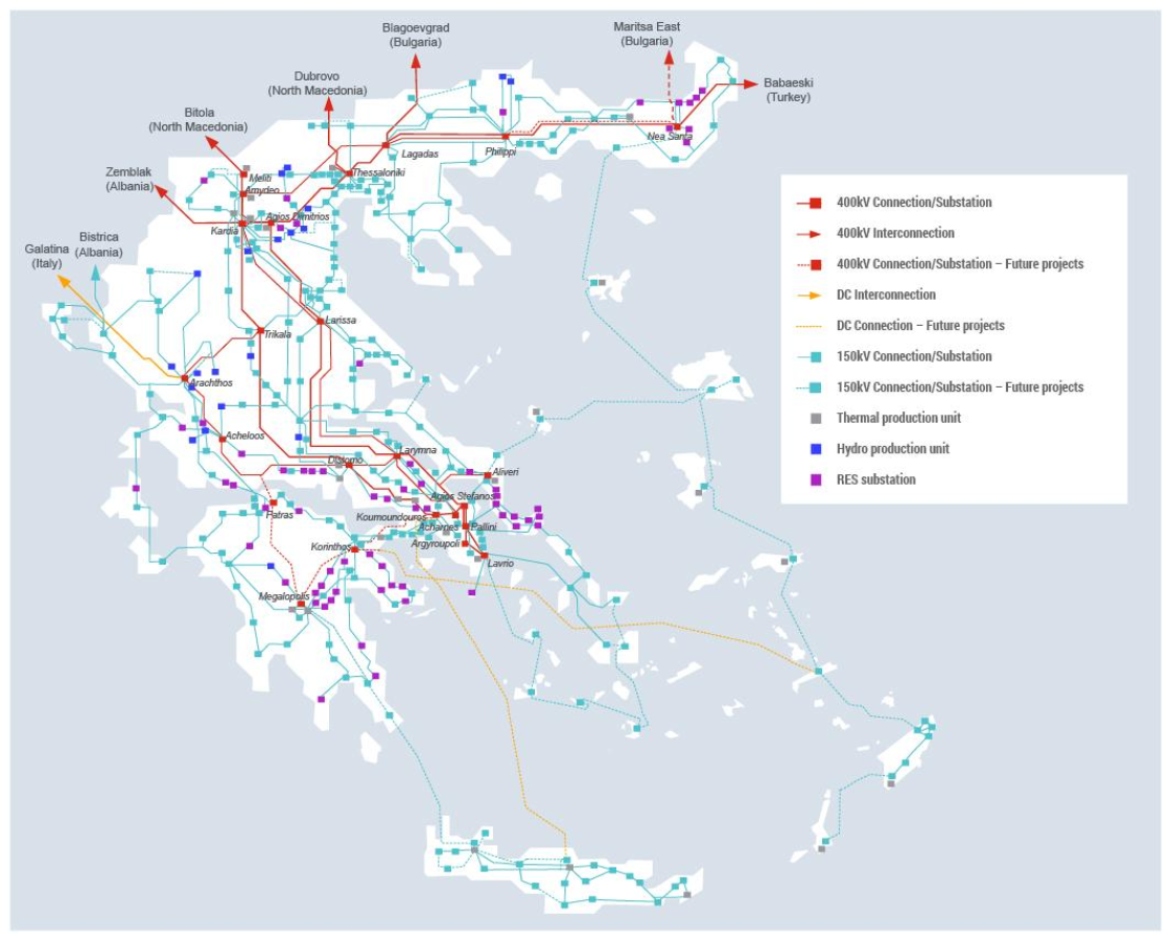

- Large-scale grid interconnection projects, including critical links to the Aegean islands

- Energy transition infrastructure, positioning the company as a backbone asset in Greece’s decarbonisation pathway

Management has emphasized that the current capital base — approximately €1 billion including state participation — is sufficient to execute the existing investment plan without operational strain.

Governance and Shareholding Shift: Post-2027 Flexibility

A key structural inflection point is expected after 2027, when the current shareholder agreement framework may be revised, particularly regarding the Chinese minority participation in ADMIE’s subsidiary structure.

Market participants view this as a potential governance simplification trigger, which could improve decision-making speed and enhance the company’s attractiveness to global index investors.

Capital Markets Timeline: London Book in Focus

According to market expectations:

- Earnings release: 15 June

- Book-building window (London): 16–18 June

- Expected fundraising size: ~€510 million

- €260m state participation

- ~€200m international tranche

- ~€50m domestic allocation

No significant disposal of treasury shares is expected due to limited availability (estimated at ~700–750k shares), which may further tighten supply dynamics during the offering.

A cornerstone investor allocation is also under discussion, though market sources suggest limited feasibility given the relatively small free float expansion relative to global demand.

Index Inclusion Upside: FTSE 25 Scenario

Post-transaction estimates place ADMIE’s market capitalization above €1.4 billion, positioning the company for potential inclusion in the FTSE 25 index at the next review cycle.

For passive and benchmark-tracking funds, this could trigger structural inflows, adding a technical support layer to the equity story beyond fundamentals.

The Institutional Upgrade Thesis (WHY INVESTORS ARE BULLISH)

The bullish argument for ADMIE is increasingly converging around a simple institutional logic: it is evolving from a domestic utility into a quasi-core infrastructure asset with European-scale visibility.

First, the revenue model is anchored in regulated returns, which in a higher-rate world have regained strategic value for institutional portfolios seeking stability, inflation linkage, and predictable cash flow duration.

Second, ADMIE sits at the center of Greece’s energy security and grid modernization cycle, with cross-regional interconnections transforming it into a structural beneficiary of EU-backed infrastructure spending.

Third, the combination of state backing + private capital access + index inclusion potential creates a rare hybrid profile: low operational volatility with expanding capital markets relevance.

Finally, the strong early-stage institutional engagement — particularly from global asset managers — suggests that ADMIE is being repositioned not as a peripheral utility, but as a core Mediterranean grid platform asset with long-term allocation potential.

If execution aligns with current expectations, ADMIE’s London transaction could mark a transition point: from a nationally anchored transmission operator to a fully integrated European infrastructure equity story, increasingly embedded in global portfolio allocation frameworks.

Source: pagenews.gr