OECD: Greece Shows Resilient Growth but Faces 4.2% Inflation Shock and Energy Exposure

Πηγή Φωτογραφίας: pixabay//OECD: Greece Shows Resilient Growth but Faces 4.2% Inflation Shock and Energy Exposure

EXECUTIVE SUMMARY – THE BIG PICTURE

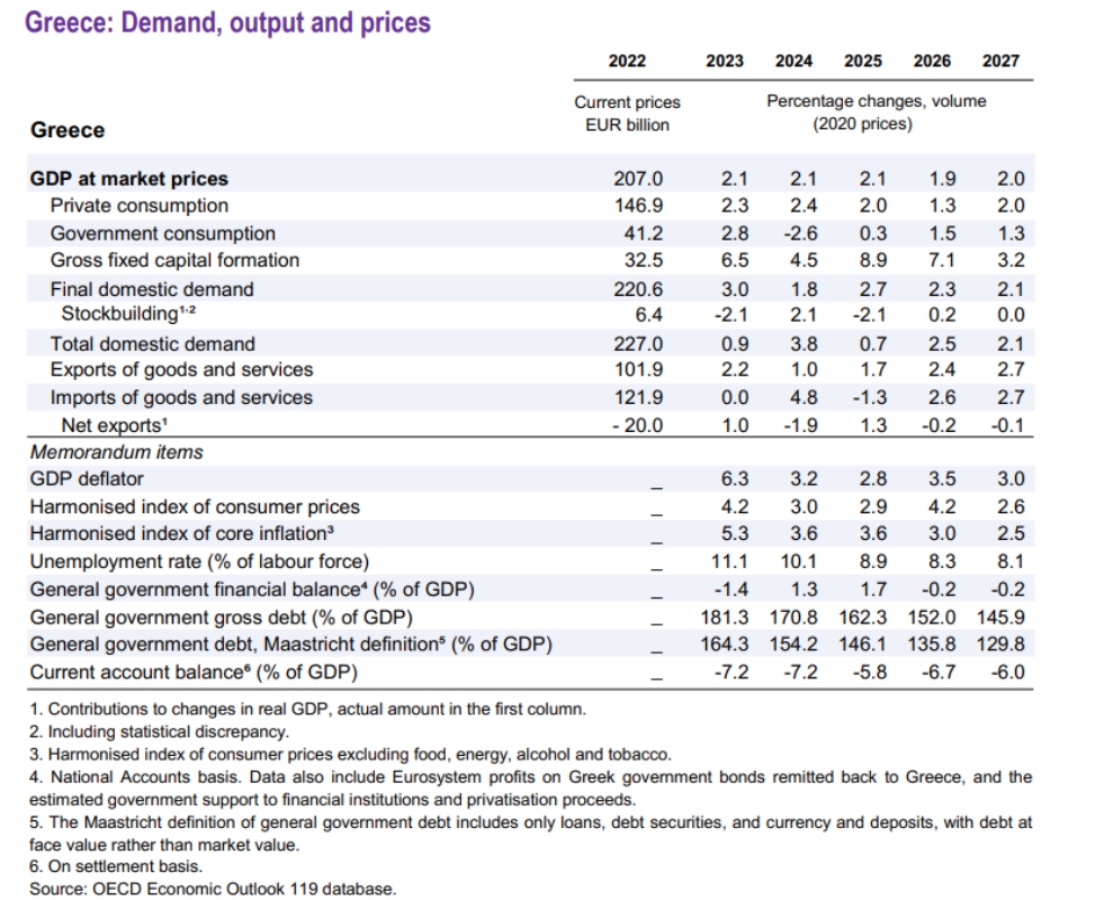

Greece enters the 2026–2027 period with a macro profile defined by stability, fiscal discipline, and external sensitivity.

The OECD projects:

- GDP growth: 1.9% (2026) and 2.0% (2027)

- Inflation: 4.2% (2026)

- Public debt: falling below 130% of GDP by 2027

- Primary surplus: stabilising above 2.5% of GDP

Behind the positive headline figures lies a structural constraint: high energy dependency and limited productive diversification.

MACRO AUTOPSY – WHAT THE NUMBERS REALLY MEAN

The OECD framework highlights three core growth engines:

1. EU funding as the main investment accelerator

RRF disbursements are expected to rise to 4.4% of GDP in 2026, acting as:

- a capex multiplier

- a catalyst for private co-investment

- a temporary buffer for weak domestic investment cycles

2. Labour market resilience vs consumption pressure

Employment growth and tax cuts support household demand, but:

- energy prices act as a structural cost burden

- consumption remains highly sensitive to external shocks

3. Exports – gradual normalization

External demand is expected to recover in late 2026, but Greece’s export base remains relatively narrow compared to peer EU economies.

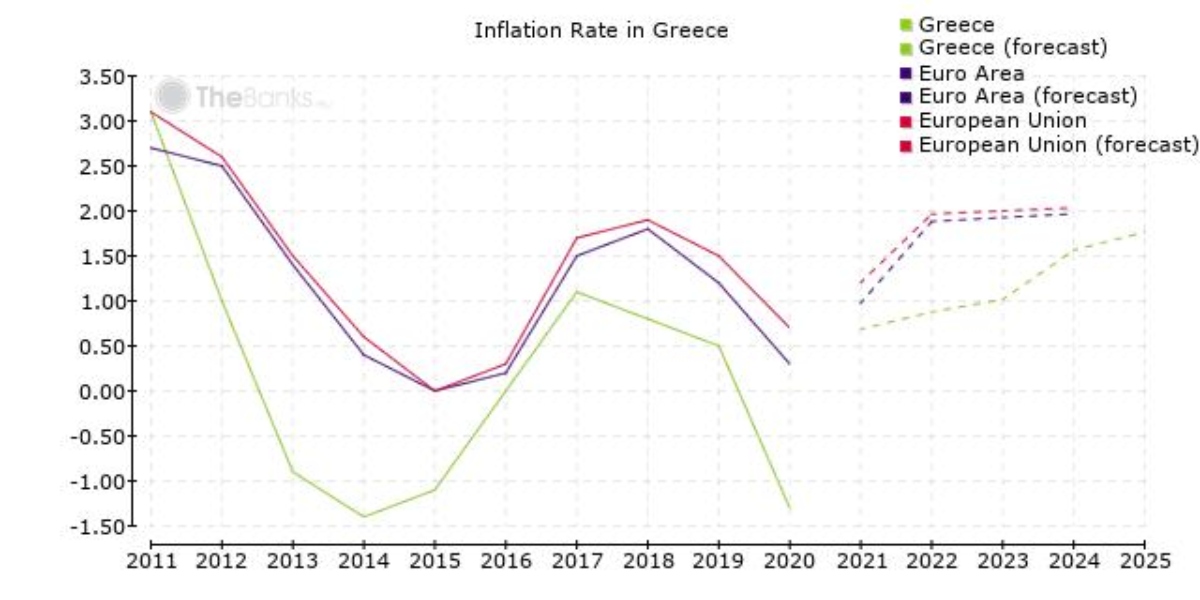

INFLATION STRESS TEST – THE KEY WEAK LINK

Inflation emerges as the most critical macro risk:

- 2.9% (2025)

- 4.2% (2026)

- 2.6% (2027)

The spike is primarily driven by:

- imported energy inflation

- oil and gas price volatility

- exposure to global supply shocks

This is effectively imported inflation rather than domestic overheating.

DEBT TRAJECTORY – FAST DELEVERAGING STORY

Debt dynamics remain Greece’s strongest macro signal:

- 146.1% (2025)

- 135.8% (2026)

- 129.8% (2027)

The OECD confirms a rapid deleveraging cycle, driven by:

- sustained primary surpluses

- nominal GDP growth

- disciplined fiscal management

POLICY STACK – OECD RECOMMENDATIONS

1. Energy transition acceleration

- simplify licensing for renewables (RES)

- reduce administrative friction for investment

- accelerate grid and permitting efficiency

2. Household energy transition support

- targeted building renovation programs

- EV adoption incentives

- gradual phase-out of fossil fuel dependency

3. Structural competitiveness reforms

- regulatory simplification for firms

- reduction of barriers for self-employed professions

- labour market upskilling and advisory systems

STRUCTURAL RISK – ENERGY DEPENDENCY EXPOSURE

A key vulnerability highlighted:

Greece relies on imported fossil fuels for approximately 93% of its total energy supply.

This creates:

- high exposure to geopolitical volatility

- imported inflation sensitivity

- external balance fragility

SCENARIO FRAMEWORK – GLOBAL UNCERTAINTY

The OECD outlines two global trajectories:

Base scenario

- global growth: 2.8% (2026) → 3.1% (2027)

- gradual easing of energy prices from mid-2026

Stress scenario

- growth falls to ~1.8% in 2027

- prolonged energy disruption

- weaker investment and labour demand

- higher financial market repricing risks

Greece’s open economy profile places it closer to the energy-sensitive tail risk zone.

FINAL TAKE – STABILITY WITHOUT STRUCTURAL TRANSFORMATION

Greece presents a dual macro identity:

- Strong fiscal credibility and declining debt

- But persistent structural dependence on imported energy and limited productivity depth

The OECD message is clear: macroeconomic stability is no longer the challenge — structural upgrading is.

The next phase of Greek economic performance will depend less on headline growth rates and more on whether investment momentum translates into a durable productivity and energy independence model.

Source: pagenews.gr

Διαβάστε όλες τις τελευταίες Ειδήσεις από την Ελλάδα και τον Κόσμο